Goat Farming Loans: Guide to Get Upto 50% Subsidy

Goat farming has become one of the most profitable livestock businesses in India. With increasing demand for goat milk, meat, and organic farming products, many farmers and young entrepreneurs are entering this sector.

However, starting or expanding a goat farming business requires proper investment and that’s exactly where goat farming loans come in.

Whether you’re a first-time farmer looking to buy your first herd or an experienced goat farmer wanting to expand your shed capacity, this comprehensive guide will walk you through everything you need to know about goat farming loans — types, eligibility, how to apply, government schemes, and tips to maximize your chances of approval and how you can get upto 50% subsidy.

What Are Goat Farming Loans?

A goat farming loan is a type of agricultural loan provided by banks, microfinance institutions, and government agencies to support goat farming activities. These loans are specially designed for individuals who want to start, manage, or expand a goat farming business. You can read here our goat farming guide.

The loan amount can be used for:

- Purchasing goats

- Building sheds and shelters

- Buying feed and medicines

- Setting up water systems

- Purchasing farming equipment

- Expanding existing goat farms

- Transportation and operational expenses

Goat farming loans fall under the broader category of animal husbandry loans or livestock loans, and many are subsidized under central and state government schemes, making them accessible even to small and marginal farmers with cheaper interest rates than normal loans.

Why Take a Goat Farming Loan?

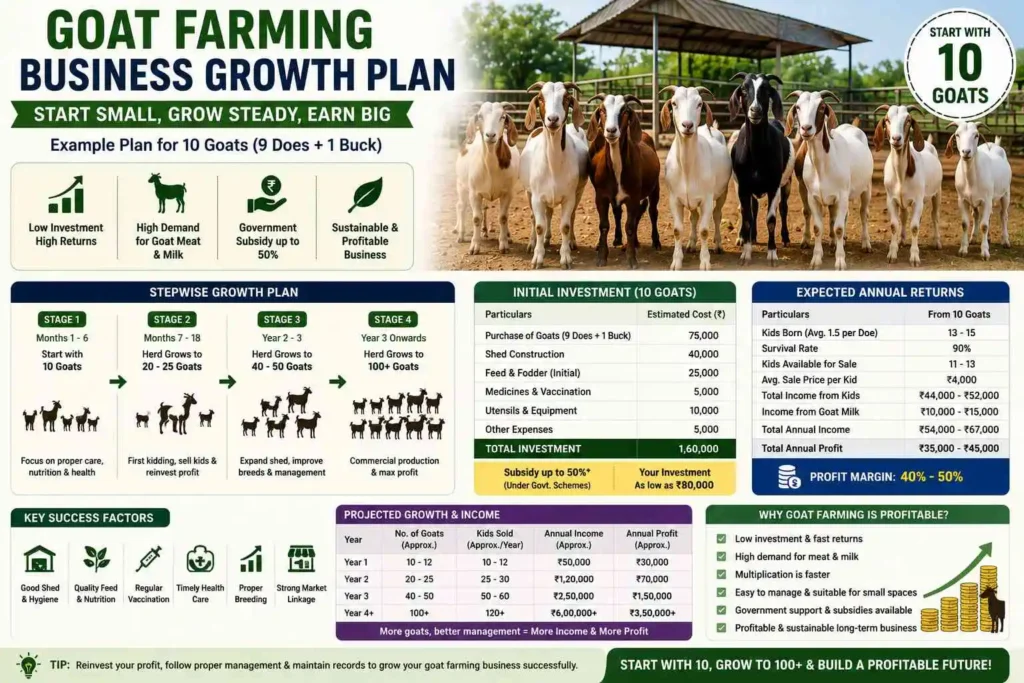

Starting a goat farm from scratch is not cheap. A flock of 20 does (female goats) with one buck (male goat) can easily cost between ₹1.5 lakh and ₹2.5 lakh in India. When you add shed construction, feeding costs, vaccinations, medicines, labor, and other operational expenses, the total investment for even a small-scale goat farming setup can cross ₹3 lakh to ₹5 lakh.

And if your goal is not just small farming but building a scalable livestock business like a modern “Kisanpreneur,” the capital requirement becomes even higher. Expanding quickly means investing in better goat breeds, larger sheds, bulk feed storage, breeding programs, and proper farm management systems. This is exactly why many aspiring farmers and agripreneurs look for goat farming loans to start and grow their business without waiting years to save enough money.

A structured goat farming loan helps you:

- Start without depleting your savings — Preserve your emergency funds while still launching the farm.

- Scale faster — Instead of slowly reinvesting profits, you can grow your herd immediately.

- Access subsidies — Many government-backed loans come with interest subventions or capital subsidies that reduce your effective borrowing cost significantly.

- Build a credit history — Successfully repaying an agricultural loan improves your CIBIL score and makes future borrowing easier.

- Formalize your farming business — Loan applications encourage better record-keeping, project planning, and business documentation.

Types of Goat Farming Loans

Understanding the different types of goat farming loans available will help you choose the right option for your situation.

1. Term Loans for Goat Farming

These are long-term loans used for capital expenditure — buying animals, building sheds, or purchasing land. Repayment periods typically range from 3 to 7 years, with a moratorium period (no repayment during the initial phase) of 6 months to 1 year while your farm becomes productive.

2. Kisan Credit Card (KCC) for Animal Husbandry

The Kisan Credit Card has been extended to include livestock and animal husbandry. Farmers can use the KCC to meet short-term working capital needs — purchasing feed, medicines, or covering daily operational expenses. The revolving credit facility makes it convenient for regular farm operations.

3. NABARD-Linked Goat Farming Loans

The National Bank for Agriculture and Rural Development (NABARD) provides refinancing support to banks offering goat farming loans. NABARD also runs direct subsidy schemes that make these loans more affordable. Banks that are NABARD-linked often offer lower interest rates and favorable repayment terms.

4. MUDRA Loans for Goat Farming

Under the Pradhan Mantri MUDRA Yojana, small goat farmers can access loans under the Shishu (up to ₹50,000), Kishor (₹50,001 to ₹5 lakh), and Tarun (₹5 lakh to ₹10 lakh) categories. These are collateral-free loans suitable for small-scale operations.

5. State Government Livestock Loan Schemes

Most Indian states have their own animal husbandry loan schemes through State Cooperative Banks, Regional Rural Banks (RRBs), and state agricultural finance corporations. These often carry heavy subsidies — especially for SC/ST farmers, women farmers, and Below Poverty Line (BPL) applicants.

Key Government Schemes Supporting Goat Farming Loans

Several central and state government schemes make goat farming loans more accessible and affordable. Here are the most important ones:

National Livestock Mission (NLM)

The NLM provides financial support for entrepreneurship development in animal husbandry, including goat farming. Under this mission, beneficiaries can receive capital subsidies of up to 50% of the project cost (higher for SC/ST/women). The scheme supports setting up of new goat farms and expansion of existing ones.

Animal Husbandry Infrastructure Development Fund (AHIDF)

With a corpus of ₹15,000 crore, AHIDF offers loans through scheduled banks for setting up animal husbandry infrastructure. Though primarily focused on processing and value addition, it supports medium and large goat farming enterprises.

NABARD’s Capital Investment Subsidy Scheme

NABARD runs a Capital Investment Subsidy Scheme for Commercial Production Units of Organic Inputs, which also extends to livestock. Under this, farmers can get subsidies that substantially reduce their loan repayment burden.

Pradhan Mantri Fasal Bima Yojana (PMFBY) – Livestock Insurance Component

While primarily a crop insurance scheme, allied programs under livestock insurance help goat farmers protect their herd against mortality risks. Insured goats often make it easier to get loans approved, as the lender’s risk is mitigated.

Eligibility Criteria for Goat Farming Loans

The eligibility rules for goat farming loans may differ from one bank or government scheme to another. However, most banks usually look for the following basic requirements:

- Age: The applicant should generally be between 18 and 65 years old.

- Occupation: The person applying should be a farmer, agricultural worker, or involved in farming-related activities such as animal husbandry or livestock farming.

- Land Ownership: Having your own land or leased land for goat farming or fodder cultivation is preferred, but it is not compulsory in every case.

- Experience: Some banks prefer applicants who already have experience in goat farming or animal husbandry, especially for larger loan amounts.

- Project Report: For loans above ₹1 lakh, banks often ask for a Detailed Project Report (DPR) explaining your goat farming plan, expenses, and expected income.

- Credit History: A good credit record with no previous loan defaults increases your chances of loan approval.

- Caste Certificate: Applicants belonging to SC/ST categories or women entrepreneurs may need to submit a caste certificate to get higher government subsidies and benefits.

Documents Required for Goat Farming Loans

To apply for goat farming loans, applicants generally need:

Identity Proof

- Aadhaar Card

- PAN Card

- Voter ID

Address Proof

- Electricity bill

- Ration card

- Passport

Financial Documents

- Bank statements

- Income proof

- Existing loan details

Agricultural Documents

- Land ownership papers

- Lease agreements

- Farm photographs

Business Documents

- Goat farming project report

- Estimated expenses

- Income projections

Proper documentation improves approval chances significantly.

How to Apply for a Goat Farming Loan: Step-by-Step

Applying for a goat farming loan can seem daunting, but breaking it into clear steps makes it manageable:

Step 1: Prepare a Detailed Project Report (DPR)

Your project report is the backbone of your loan application. It should include:

- Type and breed of goats (Boer, Sirohi, Barbari, Osmanabadi, Beetal, etc.)

- Number of animals to be purchased

- Land area and shed construction plan

- Expected production (meat, milk, kids per year)

- Revenue projections for 3–5 years

- Total project cost and fund requirements

Step 2: Gather Required Documents

Typically required documents include:

- Identity Proof (Aadhaar, Voter ID, PAN)

- Address Proof

- Land ownership or lease documents

- Passport-size photographs

- Bank statements (last 6 months)

- Caste/income certificate (if applicable)

- Project report

- Quotations for purchase of animals and materials

Step 3: Choose the Right Bank or Lender

Approach your nearest:

- Nationalized bank (SBI, Bank of Baroda, Punjab National Bank) — most have dedicated agri-loan products

- Regional Rural Bank (RRB) — often more accessible for rural farmers

- District Cooperative Bank — particularly farmer-friendly

- NABARD-linked MFI or NBFC — for smaller, collateral-free options

Step 4: Submit Your Application

Submit the completed application form along with your documents and project report. The bank’s agriculture officer may conduct a field visit to assess your proposed farm site.

Step 5: Loan Sanction and Disbursement

After verification, the bank sanctions the loan. Disbursements for animal purchases are often made directly to the seller, while construction funds may be released in phases as work progresses.

Best Banks Offering Goat Farming Loans in India

Several public sector banks, regional rural banks, and financial institutions in India provide goat farming loans to support livestock farmers and rural entrepreneurs.

1. State Bank of India

SBI is one of the most popular choices for goat farming loans because of its large rural network and agricultural financing schemes.

Key Features:

- Loans for purchasing goats, shed construction, and equipment

- Flexible repayment options

- Competitive interest rates

- Support for allied agricultural activities

SBI also works with government-backed subsidy schemes and livestock programs.

2. NABARD

NABARD does not directly give loans to farmers but supports banks by refinancing goat farming loans and subsidy schemes.

Key Benefits:

- Subsidies for eligible farmers

- Support for SHGs and rural entrepreneurs

- Lower financing burden through government schemes

Many goat farming loan schemes in India are linked with NABARD support.

3. Punjab National Bank

PNB provides agricultural and livestock loans for small and medium-scale farmers.

Benefits:

- Easy repayment options

- Loans for animal husbandry activities

- Support for rural entrepreneurs

PNB is often preferred by farmers in semi-rural and rural areas.

4. Bank of Baroda

Bank of Baroda offers financing for goat farming and other livestock businesses.

Features:

- Loans for farm setup and expansion

- Affordable interest rates

- Government subsidy support

It is considered a reliable option for new livestock entrepreneurs.

5. Canara Bank

Canara Bank provides sheep and goat rearing loans under its agricultural finance schemes.

Loan Uses:

- Purchase of goats

- Shed construction

- Feeding and maintenance expenses

Canara Bank is known for supporting small-scale livestock farmers.

6. Union Bank of India

Union Bank offers livestock loans according to NABARD guidelines.

Benefits:

- Financing for goats and sheds

- Flexible loan amounts

- Support for economically viable farming projects

The bank also offers lower-margin loans for smaller farmers.

7. IDBI Bank

IDBI Bank provides agricultural finance for goat rearing businesses.

Features:

- Loan amounts up to ₹50 lakh

- Suitable for individuals and groups

- Financing for commercial goat farming

This option is useful for entrepreneurs planning large-scale goat farming operations.

Interest Rates on Goat Farming Loans

Interest rates vary depending on the lender and the scheme under which the loan is availed:

| Loan Type | Typical Interest Rate |

| SBI Goat Farming Loan | 7% – 10.5% p.a. |

| NABARD-linked Loans | 6% – 9% p.a. |

| MUDRA Loan (Kishor/Tarun) | 9% – 12% p.a. |

| State Cooperative Bank | 5% – 8% p.a. |

| RRB Agricultural Loan | 7% – 10% p.a. |

Under the Interest Subvention Scheme, farmers who repay promptly can get an additional 3% interest rebate, bringing the effective rate as low as 4% per annum.

Loan Amounts You Can Expect

- Small unit (20–50 goats): ₹1.5 lakh – ₹5 lakh

- Medium unit (50–100 goats): ₹5 lakh – ₹15 lakh

- Large commercial unit (100+ goats): ₹15 lakh – ₹50 lakh+

The maximum loan amount depends on your project cost, repayment capacity, and the bank’s assessment.

Goat Farming Project Report for Loan Approval

A strong project report increases the chances of loan approval.

Your Project Report Should Include:

Business Overview

Explain your farming objectives and business model.

Goat Breed Information

Mention breeds such as:

- Boer

- Sirohi

- Jamunapari

- Black Bengal

Cost Estimation

Include:

- Goat purchase costs

- Shed construction

- Feed expenses

- Medical expenses

Profit Expectations

Provide realistic revenue and profit estimates.

Risk Management

Explain how you will handle:

- Diseases

- Feed shortages

- Market price fluctuations

A professional project report builds lender confidence.

Tips to Increase Your Loan Approval Chances

Getting a goat farming loan approved is not just about filling out forms. Here’s how to make your application stand out:

- Choose a high-demand breed — Banks favor breeds like Boer (meat), Barbari (dual purpose), or Beetal (milk) because they have proven market demand and higher returns.

- Get your DPR professionally prepared — Many district animal husbandry departments and NABARD offices help farmers prepare project reports for free.

- Tie up with a buyer in advance — A purchase agreement with a local meat shop, milk cooperative, or export house demonstrates market linkage and reduces lender risk.

- Insure your herd — Livestock insurance not only protects you from losses but also reassures the lender.

- Apply under a government scheme — Loans backed by NLM, NABARD, or state schemes are easier to get because they come with partial government guarantee.

- Maintain a good credit score — Clear any outstanding dues before applying. A CIBIL score above 700 makes a big difference.

- Start small, scale up — First-time farmers are sometimes advised to start with a smaller loan, repay it successfully, and then apply for a larger amount with a proven track record.

Challenges in Getting Goat Farming Loans and How to Overcome Them

Despite the availability of schemes, many farmers face obstacles:

- Lack of awareness: Many eligible farmers don’t know about subsidy schemes. Solution: Visit your nearest Krishi Vigyan Kendra (KVK) or animal husbandry department.

- Documentation hurdles: Land records, income certificates, etc. can be challenging to collect. Solution: Apply for all documents simultaneously through your local gram panchayat or block office.

- Urban bias in banks: Some bank managers in rural branches are unfamiliar with livestock loan products. Solution: Escalate to the district lead bank manager or approach NABARD’s district development manager directly.

Conclusion

Goat farming is becoming one of the most profitable agribusiness opportunities in India. However, starting and running a successful goat farm requires proper financial planning and investment. This is where goat farming loans become very helpful. These loans allow farmers and entrepreneurs to purchase goats, build sheds, arrange feed, and manage day-to-day farming expenses without putting too much financial pressure on themselves.

For the Application process of Goat farming loan read Goat farming loan apply online.

Along with financial planning, proper goat health management is also important for long-term success. Disease outbreaks can cause major losses if not handled properly. To learn more about keeping your goats healthy, you can also read our Goat Disease Management blog.

With support from banks, government schemes, and institutions like NABARD, farmers can now access funding more easily and grow their goat farming business successfully.

Disclaimer: Interest rates, loan limits, and subsidy structures mentioned in this article are indicative and subject to change. Always verify current terms with your bank or the concerned government department before applying.

Can I get a goat farming loan without owning land?

Yes, some banks provide goat farming loans even if you do not own land. Leased land or rented farm space may also be accepted, depending on the bank and loan scheme.

How much subsidy can I get on a goat farming loan?

Under government schemes like National Livestock Mission (NLM) and various state livestock schemes, eligible farmers may get subsidies of up to 25% to 50% of the project cost.

Can beginners apply for goat farming loans?

Yes, beginners can apply for goat farming loans. However, having basic knowledge or training in animal husbandry can improve the chances of loan approval.

Can I get a collateral-free goat farming loan?

Yes, small loans under schemes like MUDRA Loan and Kisan Credit Card (KCC) may be available without collateral.